We have found that a new form of debtor prison exists and this is due to excessive phone calls, emails, text messages and mail from creditors and collection agencies. These tactics can leave a person feeling afraid to answer their own phone and for some, it can cause undue stress and anxiety which can negatively affect their everyday life and ability to function at work.

Tag: debt consolidation

Why People Delay Getting Help With Their Debt

The longer an individual waits to get help with their finances, the harder it is to help as the number of options is greatly reduced. By the time most consumers come to us the only choices left are to file personal bankruptcy or consumer proposal. If you are starting to struggle financially reach out for professional assistance before things get beyond your control.

Advantages of Filing a Consumer Proposal vs. a Bankruptcy

A consumer proposal can be creative and involve the sale, over time, of assets and payment of all or a portion of the equity in those assets to your creditors. This would allow you to settle your debts through a lump-sum payment instead of having to make monthly payments.

What Happens if I Default on My Consumer Proposal

If a debtor is 3 months in arrears of monthly consumer proposal payments the consumer proposal is deemed annulled, which means that creditors can resume collection actions. There is no automatic bankruptcy if a debtor defaults on a consumer proposal.

that fails to make more than 2 payments cumulative during the Proposal will have their Proposal annulled and creditors can resume collecting their balances plus interest less any payments made. While a default on a Consumer Proposal will not automatically result in a Bankruptcy, however, the debtor cannot file another Proposal.

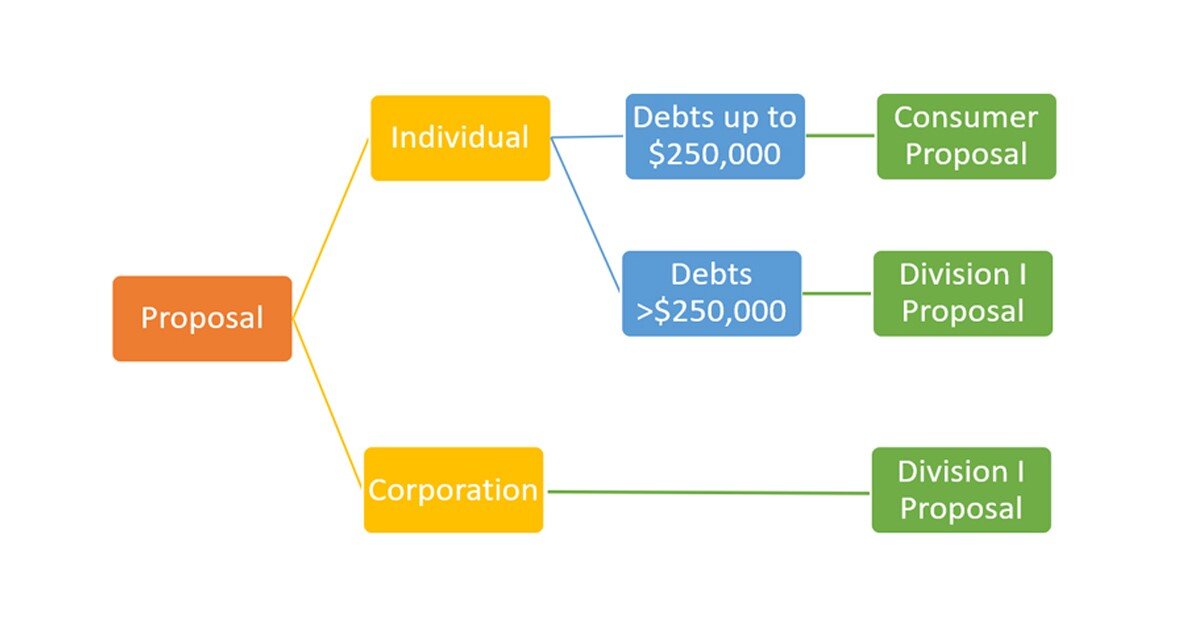

Dealing With Debt – Understanding the Two Types of Proposals

Division 1 Proposal Is when a consumer debtor owes more than $250,000 in debts, excluding the mortgage on their principal residence. If creditors don’t accept this proposal there is a deemed personal bankruptcy.

A consumer proposal is when a consumer debtor owes less than $250,000 in debts, excluding the mortgage on their principal residence. There is no deemed personal bankruptcy if the creditors reject the consumer proposal.

February 2016 – Bankruptcy & Consumer Proposal Statistics

Canada – Personal bankruptcies were down 1% and consumer proposal filings were up 9.5% as compared to the 12-months ended February 28, 2015.

New Brunswick – Personal bankruptcies were down 3.9% and consumer proposal filings were up 19.9% as compared to the 12-months ended February 28, 2015.

What Is the Bankruptcy and Insolvency Act (“BIA)

Generally speaking, the BIA is a federal statute that governs bankruptcy, proposal and receiverships in Canada. It provides relief to the honest, but unfortunate debtor from the crushing burden of debt so they can get a fresh start.

Consumer Proposal vs. Credit Counselling?

With all of the choices facing financially distressed consumers, it’s important to compare your options. The most common options are a Consumer Proposal only available through a Licensed Insolvency Trustee or a Debt Management/Repayment Plan offered by credit counselling agencies.

How Are Secured Debts Treated In Personal Bankruptcy or a Consumer Proposal?

When an individual files personal bankruptcy or a consumer proposal these loans are not always impacted and the assets can usually be kept as long as the loan payments are current and continue to be made in accordance with the credit agreement.

Can I Declare Bankruptcy If I Live Outside of The Country?

Generally speaking, under the Bankruptcy & Insolvency Act, if you reside outside of the country you can still declare bankruptcy as long as you meet certain criteria. If you are a previous Canadian resident and are have debt issues you should contact Powell Associates Ltd. to determine if you meet the criteria to file personal bankruptcy or a consumer proposal in Canada.