You can’t go bankrupt if you have no debt! Bankruptcy is a relief valve for people and companies who find themselves unable to cope with overwhelming debts. Bankruptcy is not necessarily the only option for resolving debts, but the availability of other options depends on individual circumstances. The sooner you identify and get assistance with your debts, the more options you have.

Tag: debt settlement

Advantages of Filing a Consumer Proposal vs. a Bankruptcy

A consumer proposal can be creative and involve the sale, over time, of assets and payment of all or a portion of the equity in those assets to your creditors. This would allow you to settle your debts through a lump-sum payment instead of having to make monthly payments.

What Happens if I Default on My Consumer Proposal

If a debtor is 3 months in arrears of monthly consumer proposal payments the consumer proposal is deemed annulled, which means that creditors can resume collection actions. There is no automatic bankruptcy if a debtor defaults on a consumer proposal.

that fails to make more than 2 payments cumulative during the Proposal will have their Proposal annulled and creditors can resume collecting their balances plus interest less any payments made. While a default on a Consumer Proposal will not automatically result in a Bankruptcy, however, the debtor cannot file another Proposal.

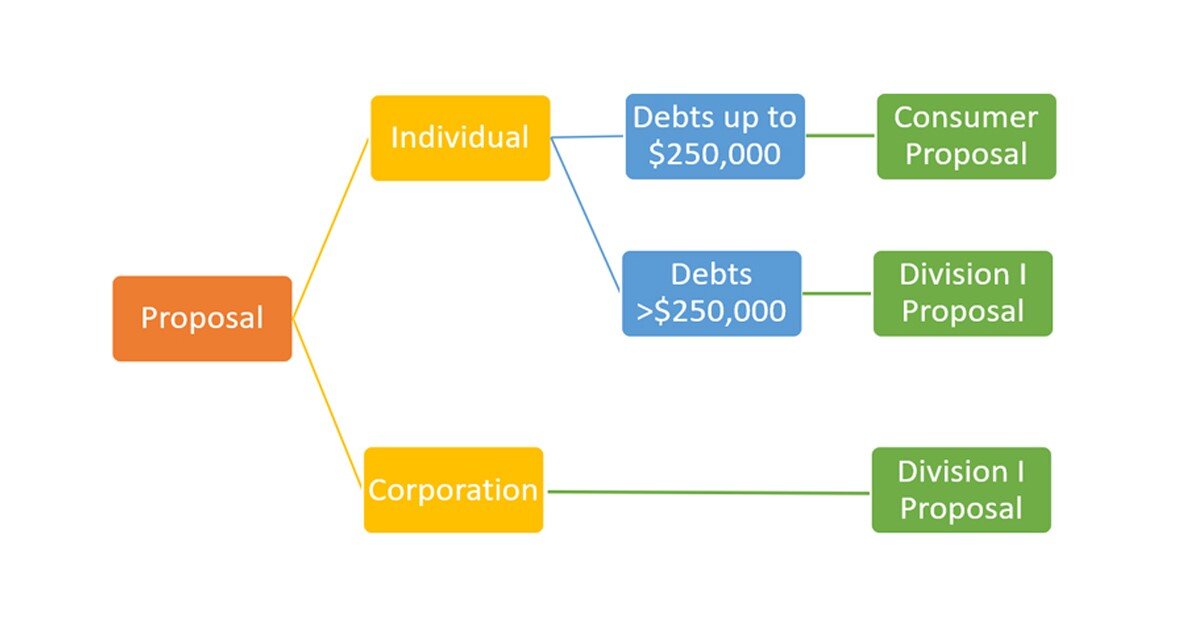

Dealing With Debt – Understanding the Two Types of Proposals

Division 1 Proposal Is when a consumer debtor owes more than $250,000 in debts, excluding the mortgage on their principal residence. If creditors don’t accept this proposal there is a deemed personal bankruptcy.

A consumer proposal is when a consumer debtor owes less than $250,000 in debts, excluding the mortgage on their principal residence. There is no deemed personal bankruptcy if the creditors reject the consumer proposal.

Consumer Proposal vs. Credit Counselling?

With all of the choices facing financially distressed consumers, it’s important to compare your options. The most common options are a Consumer Proposal only available through a Licensed Insolvency Trustee or a Debt Management/Repayment Plan offered by credit counselling agencies.

How Are Secured Debts Treated In Personal Bankruptcy or a Consumer Proposal?

When an individual files personal bankruptcy or a consumer proposal these loans are not always impacted and the assets can usually be kept as long as the loan payments are current and continue to be made in accordance with the credit agreement.

Using RRSPs to Pay Down Debt

If you are unable to keep up with your debt payments you should consult a Licensed Insolvency Trustee to discuss your options before cashing-in any of your investments. Your investment savings may be exempt from seizure so you may be able to keep them if you file for personal bankruptcy or settle your debts through a consumer proposal.

What happens If My Ex-Spouse Goes Bankrupt?

If both parties have agreed to assume responsibility for certain debts, it does not absolve them, if one of them defaults on a debt, that was granted to both parties jointly. Bankruptcy laws and family laws do not deal with assets and liabilities in the same way; there can be conflicts and unintended consequences when the two interact.

Financial Literacy – Understanding Collateral Mortgages

The mortgage process is changing and many banks have are now using collateral mortgages when you purchase or refinance your home. A collateral mortgage typically designed to secure all obligations that you owe to the bank and there is no dollar limit on the mortgage.

Do I Qualify For Bankruptcy?

Basically, if you owe at least $1,000, are unable to keep up with your monthly debt payments and do not have assets such as vehicles, house, or investments that you can sell to pay your debts in full, then you can choose to file personal bankruptcy. It is your choice whether or not to voluntarily put yourself into bankruptcy and no one can stop you.