A consumer proposal can be creative and involve the sale, over time, of assets and payment of all or a portion of the equity in those assets to your creditors. This would allow you to settle your debts through a lump-sum payment instead of having to make monthly payments.

Category: Consumer Proposals

How Will A Consumer Proposal or Bankruptcy Affect My Credit Rating?

The proposal stays on your credit file for 3 years from the date of completion. A first bankruptcy will stay on your credit report for a period of 6-7 years (depending on which Province you live in) from the date of discharge. A second bankruptcy will be reflected on the debtor’s credit report for a period of 14 years from the date of discharge.

What Happens if I Default on My Consumer Proposal

If a debtor is 3 months in arrears of monthly consumer proposal payments the consumer proposal is deemed annulled, which means that creditors can resume collection actions. There is no automatic bankruptcy if a debtor defaults on a consumer proposal.

that fails to make more than 2 payments cumulative during the Proposal will have their Proposal annulled and creditors can resume collecting their balances plus interest less any payments made. While a default on a Consumer Proposal will not automatically result in a Bankruptcy, however, the debtor cannot file another Proposal.

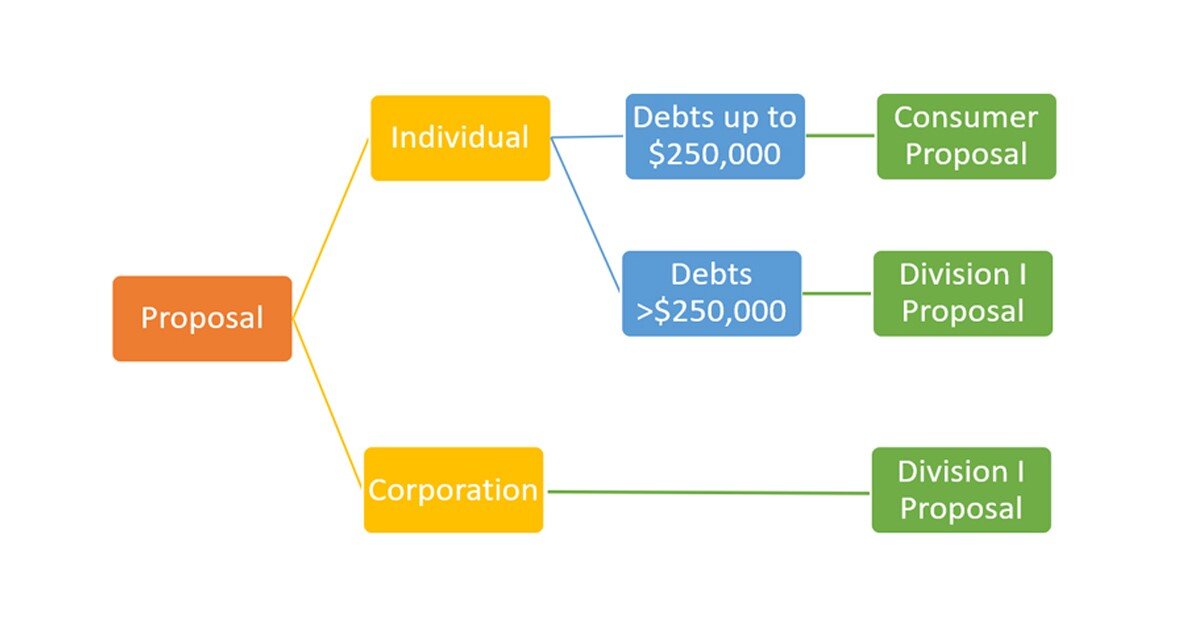

Dealing With Debt – Understanding the Two Types of Proposals

Division 1 Proposal Is when a consumer debtor owes more than $250,000 in debts, excluding the mortgage on their principal residence. If creditors don’t accept this proposal there is a deemed personal bankruptcy.

A consumer proposal is when a consumer debtor owes less than $250,000 in debts, excluding the mortgage on their principal residence. There is no deemed personal bankruptcy if the creditors reject the consumer proposal.

March 2016 – Personal Bankruptcy & Consumer Proposal Statistics

Canada – Personal bankruptcies were down 1.1% and consumer proposal filings were up 8.1% as compared to the 12-months ended March 31, 2015.

New Brunswick – Personal bankruptcies were down 5.6% and consumer proposal filings were up 16.3% as compared to the 12-months ended March 31, 2015.

Dealing With Increasing Insolvency Rates

There are lots of factors but, I think the greatest single contributor is the proliferation of easy credit combined with low levels of financial literacy. High debt levels limit financial flexibility and the ability to weather and recover from financial setbacks resulting from job loss, reduced income, illness, separation/divorce, and other life events.

February 2016 – Bankruptcy & Consumer Proposal Statistics

Canada – Personal bankruptcies were down 1% and consumer proposal filings were up 9.5% as compared to the 12-months ended February 28, 2015.

New Brunswick – Personal bankruptcies were down 3.9% and consumer proposal filings were up 19.9% as compared to the 12-months ended February 28, 2015.

The Real Cost of Vehicle Ownership

Think about the cost of ownership before you buy and then think about the cost of use and think ahead to consolidate trips, skip the trip, or car pool with friends and co-workers. The cost of vehicle ownership also needs to be considered when you choose where you live. While the cost of housing may be cheaper here in rural New Brunswick, the cost of the travel can offset the housing cost savings.

Struggling With Debt Tackle Your Finances Head On

Hiding from the reality of your financial situation will do nothing to improve it. People have a pre-disposition to hide from the truth, particularly when the truth is ugly. Unfortunately, we see this every day.

What Is the Bankruptcy and Insolvency Act (“BIA)

Generally speaking, the BIA is a federal statute that governs bankruptcy, proposal and receiverships in Canada. It provides relief to the honest, but unfortunate debtor from the crushing burden of debt so they can get a fresh start.